Key Takeaways

- Florida business law protects companies from unfair competition, contract breaches, and partner disputes.

- Acting early saves time, money, and business relationships.

- An experienced business attorney helps you assess risk and choose the right legal strategy.

Contract indemnification is defined as a contractual obligation where one party agrees to financially protect another from specific losses, claims, or liabilities, typically arising from third parties. Known formally as an indemnity clause, this provision is one of the most consequential risk allocation tools in any business contract. Understanding what is contract indemnification means understanding who pays when something goes wrong. For business owners in South Florida and beyond, a poorly drafted indemnity clause can turn a routine vendor dispute into a six-figure legal crisis. Getting this right before you sign is far less costly than fixing it after a claim lands.

What is contract indemnification and how does it work?

Contract indemnification is a risk-shifting mechanism that moves the financial burden of specific third-party claims, such as intellectual property infringement, product defects, or personal injury, from one contracting party to another. The party agreeing to cover those losses is called the indemnitor. The party receiving that protection is the indemnitee.

The definition of indemnification goes beyond simple reimbursement. A full indemnity clause typically covers defense costs, settlements, judgments, and related legal expenses. That scope makes it one of the broadest financial commitments in any commercial agreement.

Indemnification clauses appear in virtually every type of business contract, from vendor agreements and software licenses to construction contracts and commercial leases. The language varies widely, and that variation carries real financial consequences. Two contracts in the same industry can expose a business owner to dramatically different levels of risk based on a single phrase.

What are the key components of an effective indemnification clause?

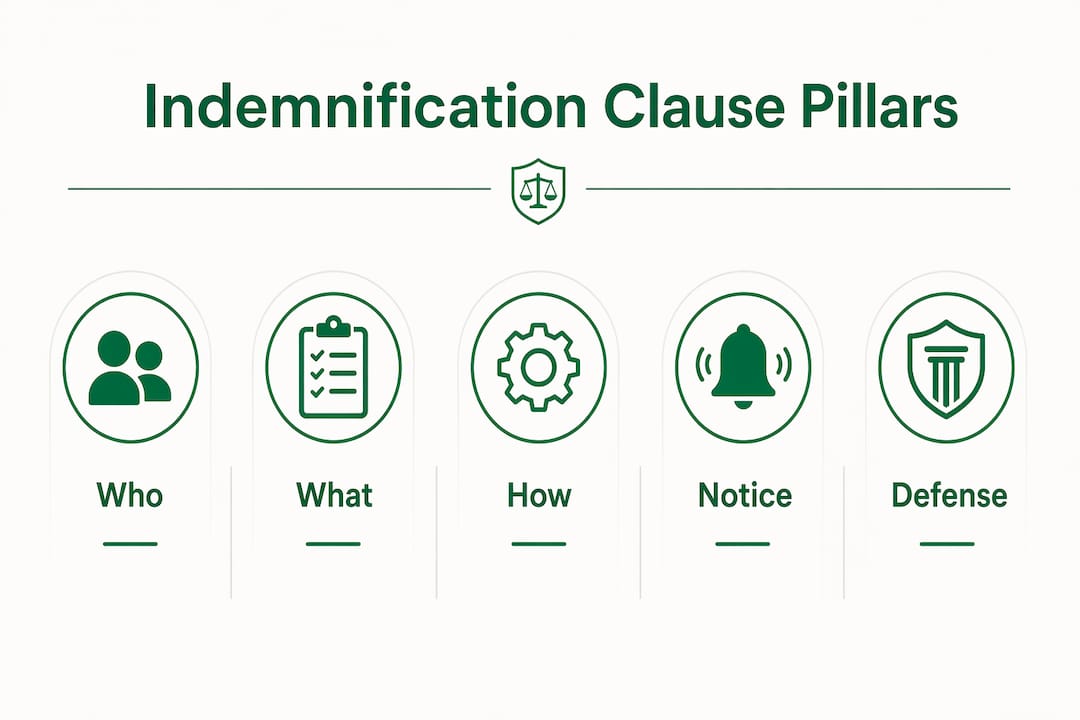

Effective indemnification clauses are built around three pillars: Who, What, and How. Missing any one of them creates gaps that courts and opposing counsel will exploit.

Who: defining the protected parties

The “Who” identifies the indemnitor (the party taking on liability) and the indemnitee (the party receiving protection). Clauses often extend protection to a party’s affiliates, officers, directors, and employees. The broader that list, the greater the indemnitor’s exposure. Business owners should read this section carefully and push back on overly broad definitions that pull in entities they have no direct relationship with.

What: the scope of covered claims

The “What” defines which claims, losses, and damages fall within the indemnity. Common categories include:

- Third-party personal injury or property damage claims

- Intellectual property infringement allegations

- Breaches of representations and warranties

- Regulatory violations or fines caused by one party’s conduct

- Product liability claims arising from defective goods or services

The scope directly determines your financial exposure. A clause covering “any and all claims” is far more dangerous than one limited to “claims arising directly from the indemnitor’s negligence.”

How: procedural requirements

The “How” covers notice obligations, defense control, and settlement consent rights. Notice periods often range from immediate to 30 days, and missing a deadline can forfeit your indemnification rights entirely. The clause should also specify who controls the defense and whether the indemnitee must consent before any settlement is reached.

Pro Tip: Always negotiate the right to approve settlements. An indemnitor who settles a claim without your consent could bind you to terms that damage your business reputation or create future liability.

Ignoring procedural rules creates expensive disputes over litigation control and notice, often costing more than the underlying claim itself.

How does the duty to defend differ from the duty to indemnify?

These two obligations sound similar but operate on completely different timelines. Confusing them is one of the most expensive mistakes a business owner can make.

-

Duty to defend. This obligation activates the moment a covered claim is filed. The indemnitor must fund and manage the legal defense throughout the entire lawsuit, including attorney fees, expert costs, and court expenses. The duty to defend is typically more costly and immediate because it runs from day one of litigation, not after a verdict.

-

Duty to indemnify. This obligation kicks in after the case resolves. Once a judgment is entered or a settlement is reached, the indemnitor reimburses the indemnitee for covered losses. It is a post-resolution payment, not an ongoing funding commitment.

-

Control over counsel. The duty to defend usually includes the right to select defense counsel. That matters because the attorney chosen shapes litigation strategy, settlement posture, and ultimately the outcome. An indemnitee who loses control of counsel selection loses meaningful input into their own defense.

-

Cash flow impact. A business without a duty-to-defend provision must fund its own defense out of pocket during litigation, sometimes for years, before any reimbursement arrives. For a small business, that cash drain can be existential.

Pro Tip: When reviewing a contract, look for both obligations explicitly stated. A clause that only mentions indemnification without addressing the duty to defend leaves you exposed during the most expensive phase of any dispute.

The distinction between these duties must appear clearly in the contract language. Vague drafting that blends the two creates disputes about when obligations begin and who controls the defense.

What are common indemnification triggers and how do they affect risk?

The trigger phrase is the language that activates the indemnity obligation. It is also the most negotiated phrase in any indemnification clause, because it determines how broadly or narrowly liability spreads.

Broad versus narrow trigger language

| Trigger Phrase | Favors | Effect |

|---|---|---|

| “Arising out of” | Indemnitee | Covers losses with any connection to the indemnitor’s conduct, even indirect |

| “Caused by” | Indemnitor | Limits liability to losses the indemnitor directly caused |

| “To the extent caused by” | Indemnitor | Proportional fault standard; indemnitor pays only their share |

| “Related to” | Indemnitee | Broad; covers tangential connections to the indemnitor’s work |

The “arising out of” trigger can hold a party liable for losses they did not directly cause. That is a significant risk for service providers and contractors whose work touches multiple parties. The “to the extent caused by” standard narrows liability to proportional fault, which protects the indemnitor but also limits the indemnitee’s recovery.

Negotiation tips for business owners:

- Push for proportional fault language if you are the indemnitor

- Seek “arising out of” language if you are the indemnitee and want broad protection

- Add a mutual indemnification structure when both parties carry comparable risk

- Review general contract terms in any standard agreement before accepting default trigger language

The most common mistake is treating indemnification as unalterable boilerplate. A single phrase change can shift hundreds of thousands of dollars in liability from one party to the other.

How do indemnification clauses interact with liability caps?

Liability caps set a ceiling on how much one party can owe the other under a contract. The critical question is whether indemnification obligations sit inside or outside that cap.

Inside versus outside the cap

| Structure | Risk to Indemnitor | Risk to Indemnitee |

|---|---|---|

| Indemnity inside the cap | Lower; total exposure is capped | Higher; recovery limited to cap amount |

| Indemnity outside the cap | Higher; no ceiling on indemnity claims | Lower; full recovery possible |

| Super-cap structure | Moderate; separate higher ceiling | Moderate; predictable recovery range |

Placing indemnity inside the standard liability cap often reduces its protection value and increases litigation risk over limits. If the cap is set at the contract value, a major third-party claim could exhaust it entirely, leaving the indemnitee with no meaningful recovery.

The super-cap is a practical solution. It sets a separate, higher financial ceiling specifically for indemnification claims, keeping indemnity outside the general cap while still giving both parties a predictable number to budget against. Negotiating super-caps offers a balance: indemnity stays outside the standard cap but still has a defined financial ceiling.

Key points to address when negotiating caps:

- Identify whether indemnity is explicitly carved out of the general liability cap

- Negotiate a super-cap amount tied to insurance coverage limits when possible

- Confirm that IP indemnification and data breach obligations carry their own carve-outs

- Assess indemnification alongside all other risk allocation terms, not in isolation

Understanding the cap structure is as important as understanding the trigger language. A perfectly drafted indemnity clause becomes nearly worthless if it is buried inside a cap that a single incident can exhaust.

Key Takeaways

Contract indemnification is a risk allocation tool that requires careful attention to trigger language, procedural rules, and cap structure to deliver real financial protection.

| Point | Details |

|---|---|

| Three-pillar structure | Every clause needs Who, What, and How to be enforceable and dispute-resistant. |

| Duty to defend timing | The duty to defend activates at filing; indemnification pays out after resolution. |

| Trigger phrase impact | “Arising out of” is broad and favors indemnitees; “to the extent caused by” is narrow and favors indemnitors. |

| Cap interaction | Indemnity inside a standard cap loses most of its value; negotiate a super-cap or carve-out. |

| Procedural compliance | Missing notice deadlines or unauthorized settlements can forfeit indemnification rights entirely. |

What I’ve learned after 20 years of reviewing indemnification clauses

Business owners consistently underestimate how much work a single indemnification clause is doing in their contracts. I have reviewed hundreds of agreements where the indemnity section was copied from a template, signed without negotiation, and later became the center of a six-figure dispute. The clause looked standard. The exposure was anything but.

The phrase “indemnify, defend, and hold harmless” appears in nearly every commercial contract. Most business owners assume those three words mean the same thing. They do not. Depending on how the rest of the clause is drafted, “hold harmless” can either overlap with indemnification or expand it in ways that create entirely new obligations. That distinction matters when a third party files a claim and both sides reach for the contract.

My practical advice: treat indemnification as a negotiation, not a formality. The contract risk management decisions you make before signing determine your exposure for the entire life of the agreement. Push back on one-sided trigger language. Confirm the duty to defend is explicit. Know whether your indemnity sits inside or outside the liability cap.

The business owners who avoid costly disputes are not the ones with the most aggressive clauses. They are the ones who understood what they signed. Getting legal guidance before signing a contract with a broad indemnity obligation costs a fraction of what it costs to litigate one.

— Matthew

Fornarolegal helps Florida business owners get indemnification right

Indemnification clauses are where contract disputes are won or lost, often before either party realizes a problem exists. Fornarolegal works with small businesses, startups, and entrepreneurs across South Florida to review, negotiate, and draft indemnification provisions that reflect your actual risk profile.

Matthew Fornaro brings over 20 years of court-tested experience to every contract review. Whether you are signing a vendor agreement, a commercial lease, or a service contract with a broad indemnity obligation, Fornarolegal identifies the clauses that create real exposure and helps you negotiate terms that protect your business. Early legal guidance is the most cost-effective way to avoid the disputes that indemnification clauses are supposed to prevent. Contact Fornarolegal before you sign, not after a claim arrives.

FAQ

What is the basic definition of indemnification in a contract?

Indemnification is a contractual obligation where one party agrees to compensate another for specific losses, claims, or liabilities, typically those arising from third parties. It covers defense costs, settlements, and judgments within the defined scope.

Is indemnification necessary in every business contract?

Indemnification is not legally required in every contract, but it is a critical risk management tool in any agreement where one party’s actions could expose the other to third-party claims. Skipping it leaves both parties without a clear framework for who pays when something goes wrong.

What is the difference between indemnification and hold harmless?

Indemnification requires one party to compensate another for covered losses. “Hold harmless” sometimes overlaps with indemnification but can also prevent the indemnitee from being held liable in the first place. The practical difference depends entirely on how the clause is drafted.

How does an indemnification clause interact with insurance?

Indemnification clauses and insurance policies work together but are not interchangeable. A contract can require indemnification even when insurance does not cover the specific claim, which is why aligning indemnity obligations with your actual insurance coverage limits is a standard part of contract negotiation.

Can indemnification clauses be negotiated?

Indemnification clauses are highly negotiable. Trigger language, scope, procedural requirements, and cap structures are all open to negotiation. Accepting default language without review is one of the most common and costly mistakes business owners make.

Recommended

- How to Protect Business Interests in Contracts: A Legal Guide » Matthew Fornaro, P.A. Coral Springs Parkland Business Law

- How to Protect Your Growing Florida Business from Contract, Ownership, and Lease Risk » Matthew Fornaro, P.A. Coral Springs Parkland Business Law

- Breach of Contract Lawyer for Business » Matthew Fornaro, P.A. Coral Springs Parkland Business Law

- Business Contract Dispute Resolution Tips That Work » Matthew Fornaro, P.A.