Key Takeaways

- Florida business law protects companies from unfair competition, contract breaches, and partner disputes.

- Acting early saves time, money, and business relationships.

- An experienced business attorney helps you assess risk and choose the right legal strategy.

A business partnership agreement is a legally binding document that defines each partner’s roles, ownership stake, profit sharing, and dispute resolution process. Without one, Florida’s default partnership statutes take over. Those defaults assume equal profit sharing and equal management authority regardless of how much each partner actually contributes. For South Florida entrepreneurs ready to draft a business partnership agreement, that gap between assumption and reality is where most disputes begin. This guide covers every core element, the step-by-step drafting process, and the most common mistakes that turn promising partnerships into expensive legal battles.

What are the essential components of a partnership agreement?

A well-structured partnership agreement covers seven core sections. Each one closes a specific gap that default state law leaves open.

- Partner identification and roles. Name every partner, define their title, and list their specific responsibilities. Vague role descriptions are the single most common source of early conflict.

- Capital contributions. Specify the dollar amount, asset type, and timeline for each partner’s contribution. A partner who promises $50,000 in equipment but delivers it six months late creates real cash flow damage.

- Ownership percentages. State each partner’s ownership share as a fixed percentage. This number governs voting rights, profit allocation, and buyout calculations.

- Profit and loss sharing. Profit distribution terms can follow ownership percentages or be split equally regardless of stakes. Decide the method and the draw schedule upfront to protect cash flow.

- Binding authority limits. Without explicit limits, any partner can legally commit the partnership to contracts or debt. That exposure reaches every partner’s personal assets. Define dollar thresholds and approval requirements clearly.

- Buy-sell provisions. Address what happens when a partner wants to exit, becomes disabled, or dies. Withdrawal and death provisions should include a valuation method and, ideally, a life insurance requirement naming partners as beneficiaries.

- Dispute resolution. Require mediation before litigation. Many South Florida entrepreneurs also include binding arbitration as a second step. A clear protocol keeps disputes out of court and keeps the business running.

Pro Tip: Include a decision-making deadlock clause. If two 50/50 partners cannot agree, the agreement should specify a tiebreaker process, such as a neutral third-party mediator, rather than leaving the business paralyzed.

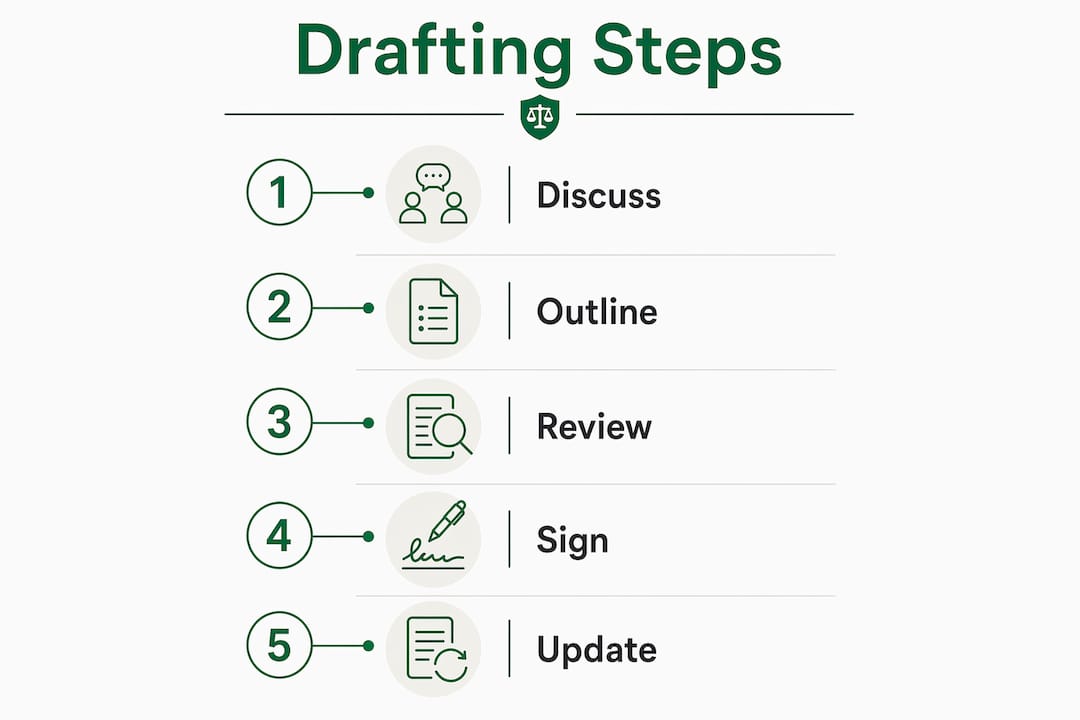

How do you draft a partnership agreement step by step?

The drafting process has six distinct stages. Skipping any one of them creates a gap that surfaces later as a dispute or a compliance problem.

-

Agree on goals, roles, and contributions. Before writing a single clause, sit down with your partner and document your shared vision, each person’s expected time commitment, and what each party brings to the table. Most partnership disputes stem from misaligned expectations over business vision and roles. Resolving those differences on paper before money changes hands is far cheaper than resolving them in court.

-

Choose your partnership structure. Florida recognizes General Partnerships, Limited Partnerships, and Limited Liability Partnerships (LLPs). Each carries different liability exposure and tax treatment. A General Partnership offers simplicity but exposes all partners to unlimited personal liability. An LLP limits liability for each partner’s individual misconduct while keeping pass-through taxation.

-

Draft the agreement to reflect Florida law. State-specific rules govern default profit sharing, dissolution procedures, and partner authority. Your agreement must either adopt or explicitly override those defaults. Generic online templates frequently miss Florida-specific requirements, leaving partners exposed.

-

Register your trade name and meet tax obligations. Partnership formation and business registration are two separate legal steps. File a DBA (doing business as) or fictitious name registration with the Florida Division of Corporations if you operate under a name other than the partners’ legal names. Obtain an EIN from the IRS for tax filing purposes.

-

Open a dedicated business bank account. Mixing personal and business funds destroys the liability separation you worked to create. Open the account in the partnership’s name immediately after registration.

-

Have legal counsel review the agreement before signing. DIY templates often fail to address complex liability, tax consequences, and custom provisions needed for growing businesses. An attorney review catches gaps before they become binding problems.

The table below summarizes the structure choices South Florida entrepreneurs most commonly face.

| Structure | Liability | Best for |

|---|---|---|

| General Partnership | Unlimited personal liability | Simple, low-risk ventures |

| Limited Partnership | Limited for passive partners | Investor-backed businesses |

| LLP | Limited per-partner liability | Professional service firms |

What are the most common mistakes when drafting a partnership contract?

South Florida entrepreneurs repeat the same errors across industries. Knowing them in advance is the fastest way to avoid them.

-

Relying on a verbal agreement. A handshake deal is legally a general partnership in Florida. Partnerships form automatically when two or more people work together for profit. The problem is that without a written agreement, Florida’s default rules control everything, and those defaults rarely match what the partners actually intended.

-

Leaving binding authority undefined. Unregulated partner authority is one of the most overlooked risks in partnership agreements. One partner signing a $200,000 lease without the other’s knowledge is legally binding on both. Set clear dollar thresholds and require written approval above them.

-

Ignoring exit and succession planning. Failing to include buy-sell provisions forces partners into court when one wants to leave or passes away. A predetermined valuation method, such as a multiple of EBITDA or a third-party appraisal, removes the guesswork and the conflict.

-

Skipping dispute resolution clauses. Litigation is expensive and slow. A mediation and arbitration clause gives partners a faster, lower-cost path to resolution. Without one, a single disagreement can shut down operations for months.

-

Using a generic template for a complex business. Off-the-shelf templates work for the simplest arrangements. Licensed professionals, businesses with significant assets, or ventures with unequal contributions need custom provisions. The cost of professional drafting is a fraction of the cost of a single dispute.

Pro Tip: Ask your attorney to include a “material change” trigger in the agreement. Any event that significantly alters the business, such as adding a new partner, taking on major debt, or changing the core business model, should automatically require a formal agreement review.

How do you keep a partnership agreement current?

A signed agreement is not a permanent document. Business conditions change, and an outdated agreement creates the same risks as no agreement at all.

- Schedule annual reviews. Set a fixed date each year to read through the agreement together. Periodic reviews reduce dispute risk by catching misalignments before they escalate. Treat it the same way you treat an annual financial audit.

- Document all amendments formally. Every change needs a written addendum signed by all partners. Verbal modifications are unenforceable and create conflicting accounts of what was agreed.

- Use the agreement’s dispute protocol first. When a conflict arises, follow the mediation or arbitration steps written into the agreement before escalating. Partners who skip this step often waive contractual rights. Understanding digital evidence in civil disputes can also matter if a conflict involves emails, texts, or electronic records.

- Consult legal counsel for major changes. Adding a partner, restructuring ownership, or entering a new market all require legal review. An attorney can confirm that the amendment is enforceable and consistent with current Florida law.

- Keep signed copies accessible. Store executed copies in a secure location that all partners can access. A dispute over what the agreement actually says is avoidable with proper document management.

Key Takeaways

A written partnership agreement is the single most effective tool for preventing costly disputes and protecting every partner’s personal assets under Florida law.

| Point | Details |

|---|---|

| Written agreement is critical | Florida default rules assume equal shares regardless of actual contributions, creating built-in conflict. |

| Seven core sections | Every agreement needs partner IDs, capital terms, ownership percentages, profit sharing, authority limits, exit provisions, and dispute resolution. |

| Follow a six-step process | Agree on goals, choose a structure, draft to Florida law, register, open a business account, and get legal review. |

| Avoid the top five mistakes | Verbal agreements, undefined authority, no exit plan, no dispute clause, and generic templates all create serious exposure. |

| Review and update regularly | Annual reviews and formal amendments keep the agreement enforceable as the business evolves. |

What I’ve learned from watching South Florida partnerships break down

The disputes I see most often do not start with bad intentions. They start with two people who genuinely trust each other and decide that writing everything down feels unnecessary. That trust is real. The problem is that trust does not define what happens when one partner wants to sell and the other does not, or when one partner stops showing up but still owns 50% of the business.

The agreements that hold up are not the longest ones. They are the ones drafted after an honest conversation about the hard questions: What happens if this fails? What if one of us gets sick? What if we disagree on a major hire? Those conversations are uncomfortable, but they are far less uncomfortable than a lawsuit.

One pattern I see repeatedly in South Florida is partners who invest heavily before formalizing anything. By the time they want an agreement, there is already money in, emotions are high, and every clause feels like an accusation. The right time to protect your Florida business from partnership disputes is before the first dollar is spent, not after the first argument.

My practical advice: treat the drafting process as a business planning exercise, not a legal formality. If you and your partner cannot agree on the terms of the agreement, that is important information. It tells you something about how you will handle disagreements when real money is at stake.

— Matthew

How Fornarolegal helps South Florida entrepreneurs get it right

Drafting a partnership agreement without legal guidance is a calculated risk. The gaps you miss today become the disputes you pay to resolve tomorrow.

Fornarolegal works with entrepreneurs and small business owners across South Florida to draft, review, and enforce partnership agreements that reflect how the business actually operates. With over 20 years of court-tested experience, Matthew Fornaro helps partners address the hard questions before they become legal problems. Early legal guidance is consistently the most cost-effective investment a new partnership can make. Whether you are starting fresh or formalizing an existing arrangement, Fornarolegal provides the practical, specific counsel that protects your interests from day one.

FAQ

What is a business partnership agreement?

A business partnership agreement is a written contract that defines each partner’s roles, ownership percentage, profit sharing, and dispute resolution process. Without one, Florida’s default partnership statutes control those terms automatically.

Is a written partnership agreement legally required in Florida?

A written agreement is not legally required to form a general partnership in Florida, but default state rules assume equal profit sharing and equal authority regardless of actual contributions. A written agreement overrides those defaults and protects every partner.

What happens if a partner wants to leave the business?

Without buy-sell provisions in the agreement, a partner’s exit can trigger forced dissolution under Florida law. A properly drafted agreement includes a valuation method and a buyout process that keeps the business operating.

Can I use a free partnership agreement template?

Free templates cover basic terms but often miss complex provisions for liability, taxes, and custom arrangements. Professional legal review is recommended for any partnership involving significant assets, unequal contributions, or licensed activities.

How often should a partnership agreement be updated?

A partnership agreement should be reviewed at least once a year and updated whenever a major business change occurs, such as adding a partner, restructuring ownership, or taking on significant debt. Formal written amendments signed by all partners are required to make changes enforceable.

Recommended

- What to Include in a Partnership Agreement: 2026 Guide » Matthew Fornaro, P.A. Coral Springs Parkland Business Law

- Before You Add a Partner, Investor, or New Owner in Florida: A Legal Checklist for SMBs » Matthew Fornaro, P.A. Coral Springs Parkland Business Law

- How to Structure a 50/50 Business Partnership in Florida » Matthew Fornaro, P.A. Coral Springs Parkland Business Law

- Resolve Business Partner Disputes in Florida: 2026 Guide » Matthew Fornaro, P.A.